How Tokenization Technology Can Protect You from Fraud

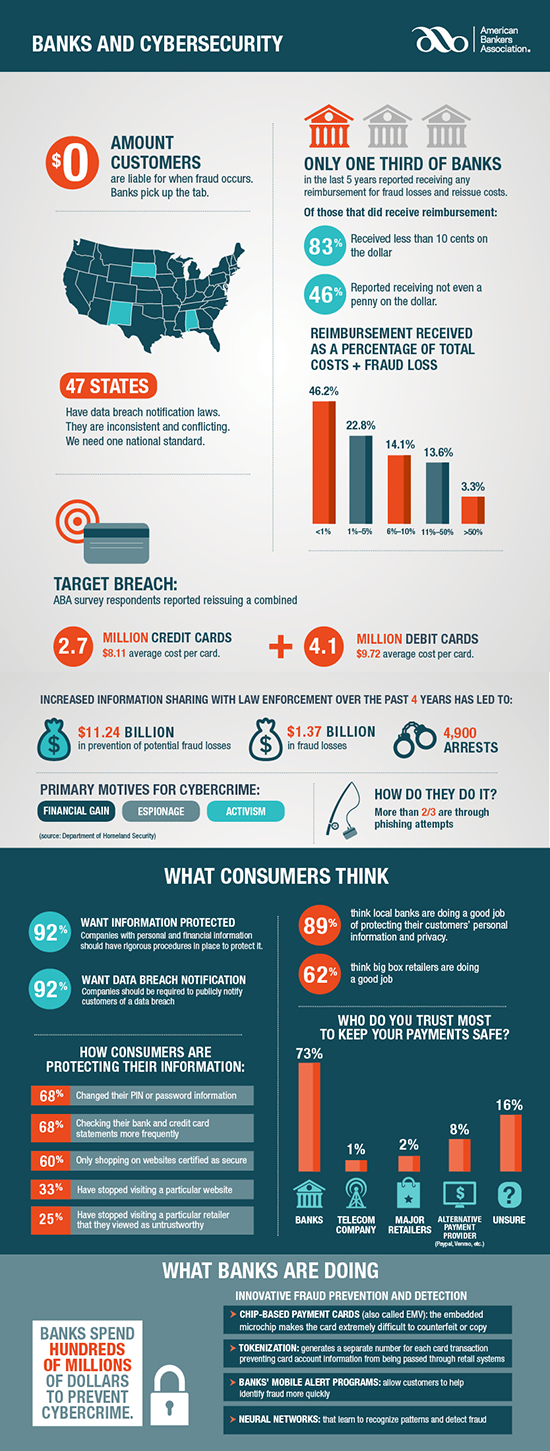

Banks and Cybersecurity

How to Get Your Free Credit Report

Courtesy of consumer.ftc.gov

Courtesy of consumer.ftc.gov

The Fair Credit Reporting Act (FCRA) requires each of the nationwide credit reporting companies — Equifax, Experian, and TransUnion — to provide you with a free copy of your credit report, at your request, once every 12 months. The FCRA promotes the accuracy and privacy of information in the files of the nation’s credit reporting companies. The Federal Trade Commission (FTC), the nation’s consumer protection agency, enforces the FCRA with respect to credit reporting companies.

A credit report includes information on where you live, how you pay your bills, and whether you’ve been sued or have filed for bankruptcy. Nationwide credit reporting companies sell the information in your report to creditors, insurers, employers, and other businesses that use it to evaluate your applications for credit, insurance, employment, or renting a home.

Here are the details about your rights under the FCRA, which established the free annual credit report program.

Q: How do I order my free report?

The three nationwide credit reporting companies have set up a central website, a toll-free telephone number, and a mailing address through which you can order your free annual report.

To order, visit annualcreditreport.com, call 1-877-322-8228. Or complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281. Do not contact the three nationwide credit reporting companies individually. They are providing free annual credit reports only through annualcreditreport.com, 1-877-322-8228 or mailing to Annual Credit Report Request Service.

You may order your reports from each of the three nationwide credit reporting companies at the same time, or you can order your report from each of the companies one at a time. The law allows you to order one free copy of your report from each of the nationwide credit reporting companies every 12 months.

A Warning About “Imposter” Websites

Only one website is authorized to fill orders for the free annual credit report you are entitled to under law — annualcreditreport.com. Other websites that claim to offer “free credit reports,” “free credit scores,” or “free credit monitoring” are not part of the legally mandated free annual credit report program. In some cases, the “free” product comes with strings attached. For example, some sites sign you up for a supposedly “free” service that converts to one you have to pay for after a trial period. If you don’t cancel during the trial period, you may be unwittingly agreeing to let the company start charging fees to your credit card.

Some “imposter” sites use terms like “free report” in their names; others have URLs that purposely misspell annualcreditreport.com in the hope that you will mistype the name of the official site. Some of these “imposter” sites direct you to other sites that try to sell you something or collect your personal information.

Annualcreditreport.com and the nationwide credit reporting companies will not send you an email asking for your personal information. If you get an email, see a pop-up ad, or get a phone call from someone claiming to be from annualcreditreport.com or any of the three nationwide credit reporting companies, do not reply or click on any link in the message. It’s probably a scam. Forward any such email to the FTC at spam@uce.gov.

Q: What information do I need to provide to get my free report?

A: You need to provide your name, address, Social Security number, and date of birth. If you have moved in the last two years, you may have to provide your previous address. To maintain the security of your file, each nationwide credit reporting company may ask you for some information that only you would know, like the amount of your monthly mortgage payment. Each company may ask you for different information because the information each has in your file may come from different sources.

Q: Why do I want a copy of my credit report?

A: Your credit report has information that affects whether you can get a loan — and how much you will have to pay to borrow money. You want a copy of your credit report to:

- make sure the information is accurate, complete, and up-to-date before you apply for a loan for a major purchase like a house or car, buy insurance, or apply for a job.

- help guard against identity theft. That’s when someone uses your personal information — like your name, your Social Security number, or your credit card number — to commit fraud. Identity thieves may use your information to open a new credit card account in your name. Then, when they don’t pay the bills, the delinquent account is reported on your credit report. Inaccurate information like that could affect your ability to get credit, insurance, or even a job.

Q: How long does it take to get my report after I order it?

A: If you request your report online at annualcreditreport.com, you should be able to access it immediately. If you order your report by calling toll-free 1-877-322-8228, your report will be processed and mailed to you within 15 days. If you order your report by mail using the Annual Credit Report Request Form, your request will be processed and mailed to you within 15 days of receipt.

Whether you order your report online, by phone, or by mail, it may take longer to receive your report if the nationwide credit reporting company needs more information to verify your identity.

Q: Are there any other situations where I might be eligible for a free report?

A: Under federal law, you’re entitled to a free report if a company takes adverse action against you, such as denying your application for credit, insurance, or employment, and you ask for your report within 60 days of receiving notice of the action. The notice will give you the name, address, and phone number of the credit reporting company. You’re also entitled to one free report a year if you’re unemployed and plan to look for a job within 60 days; if you’re on welfare; or if your report is inaccurate because of fraud, including identity theft. Otherwise, a credit reporting company may charge you a reasonable amount for another copy of your report within a 12-month period.

To buy a copy of your report, contact:

- Equifax:1-800-685-1111; equifax.com

- Experian: 1-888-397-3742; experian.com

- TransUnion: 1-800-916-8800; transunion.com

Q: Should I order a report from each of the three nationwide credit reporting companies?

A: It’s up to you. Because nationwide credit reporting companies get their information from different sources, the information in your report from one company may not reflect all, or the same, information in your reports from the other two companies. That’s not to say that the information in any of your reports is necessarily inaccurate; it just may be different.

Q: Should I order my reports from all three of the nationwide credit reporting companies at the same time?

A: You may order one, two, or all three reports at the same time, or you may stagger your requests. It’s your choice. Some financial advisors say staggering your requests during a 12-month period may be a good way to keep an eye on the accuracy and completeness of the information in your reports.

Q: What if I find errors — either inaccuracies or incomplete information — in my credit report?

A: Under the FCRA, both the credit reporting company and the information provider (that is, the person, company, or organization that provides information about you to a consumer reporting company) are responsible for correcting inaccurate or incomplete information in your report. To take full advantage of your rights under this law, contact the credit reporting company and the information provider.

1. Tell the credit reporting company, in writing, what information you think is inaccurate.

Credit reporting companies must investigate the items in question — usually within 30 days — unless they consider your dispute frivolous. They also must forward all the relevant data you provide about the inaccuracy to the organization that provided the information. After the information provider receives notice of a dispute from the credit reporting company, it must investigate, review the relevant information, and report the results back to the credit reporting company. If the information provider finds the disputed information is inaccurate, it must notify all three nationwide credit reporting companies so they can correct the information in your file.

When the investigation is complete, the credit reporting company must give you the written results and a free copy of your report if the dispute results in a change. (This free report does not count as your annual free report.) If an item is changed or deleted, the credit reporting company cannot put the disputed information back in your file unless the information provider verifies that it is accurate and complete. The credit reporting company also must send you written notice that includes the name, address, and phone number of the information provider.

2. Tell the creditor or other information provider in writing that you dispute an item. Many providers specify an address for disputes. If the provider reports the item to a credit reporting company, it must include a notice of your dispute. And if you are correct — that is, if the information is found to be inaccurate — the information provider may not report it again.

Q: What can I do if the credit reporting company or information provider won’t correct the information I dispute?

A: If an investigation doesn’t resolve your dispute with the credit reporting company, you can ask that a statement of the dispute be included in your file and in future reports. You also can ask the credit reporting company to provide your statement to anyone who received a copy of your report in the recent past. You can expect to pay a fee for this service.

If you tell the information provider that you dispute an item, a notice of your dispute must be included any time the information provider reports the item to a credit reporting company.

Q: How long can a credit reporting company report negative information?

A: A credit reporting company can report most accurate negative information for seven years and bankruptcy information for 10 years. There is no time limit on reporting information about criminal convictions; information reported in response to your application for a job that pays more than $75,000 a year; and information reported because you’ve applied for more than $150,000 worth of credit or life insurance. Information about a lawsuit or an unpaid judgment against you can be reported for seven years or until the statute of limitations runs out, whichever is longer.

Q: Can anyone else get a copy of my credit report?

A: The FCRA specifies who can access your credit report. Creditors, insurers, employers, and other businesses that use the information in your report to evaluate your applications for credit, insurance, employment, or renting a home are among those that have a legal right to access your report.

Q: Can my employer get my credit report?

A: Your employer can get a copy of your credit report only if you agree. A credit reporting company may not provide information about you to your employer, or to a prospective employer, without your written consent.

SEC Shuts Down $600 Million Online Pyramid and Ponzi Scheme

Courtesy U.S. Security and Exchange Commission

Washington, D.C., Aug. 17, 2012 – The Securities and Exchange Commission today announced fraud charges and an emergency asset freeze to halt a $600 million Ponzi scheme on the verge of collapse. The emergency action assures that victims can recoup more of their money and potentially avoid devastating losses.

The SEC alleges that online marketer Paul Burks of Lexington, N.C. and his company Rex Venture Group have raised money from more than one million Internet customers nationwide and overseas through the website ZeekRewards.com, which they began in January 2011.

According to the SEC’s complaint filed in federal court in Charlotte, N.C., customers were offered several ways to earn money through the ZeekRewards program, two of which involved purchasing securities in the form of investment contracts. These securities offerings were not registered with the SEC as required under the federal securities laws.

The SEC alleges that investors were collectively promised up to 50 percent of the company’s daily net profits through a profit sharing system in which they accumulate rewards points that they can use for cash payouts. However, the website fraudulently conveyed the false impression that the company was extremely profitable when, in fact, the payouts to investors bore no relation to the company’s net profits. Most of ZeekRewards’ total revenues and the “net profits” paid to investors have been comprised of funds received from new investors in classic Ponzi scheme fashion.

“The obligations to investors drastically exceed the company’s cash on hand, which is why we need to step in quickly, salvage whatever funds remain and ensure an orderly and fair payout to investors,” said Stephen Cohen, an Associate Director in the SEC’s Division of Enforcement. “ZeekRewards misused the power of the Internet and lured investors by making them believe they were getting an opportunity to cash in on the next big thing. In reality, their cash was just going to the earlier investor.”

The SEC’s complaint alleges that the scheme is teetering on collapse with investor funds at risk of dissipation without its emergency enforcement action. Last month, ZeekRewards brought in approximately $162 million while total investor cash payouts were approximately $160 million. If customers continue to increasingly elect to receive cash payouts rather than reinvesting their money to reach higher levels of rewards points, ZeekRewards’ cash outflows would eventually exceed its total revenue.

Burks has agreed to settle the SEC’s charges against him without admitting or denying the allegations, and agreed to cooperate with a court-appointed receiver.

According to the SEC’s complaint, ZeekRewards has paid out nearly $375 million to investors to date and holds approximately $225 million in investor funds in 15 foreign and domestic financial institutions. Those funds will be frozen under the emergency asset freeze granted by the court at the SEC’s request. Meanwhile, Burks has personally siphoned several million dollars of investors’ funds while operating Rex Venture and ZeekRewards, and he distributed at least $1 million to family members. Burks has agreed to relinquish his interest in the company and its assets plus pay a $4 million penalty. Additionally, the court has appointed a receiver to collect, marshal, manage and distribute remaining assets for return to harmed investors.

The SEC’s investigation was conducted by Brian M. Privor and Alfred C. Tierney in the SEC’s Enforcement Division in Washington D.C. The SEC acknowledges the assistance of the Quebec Autorite des Marches Financiers and the Ontario Securities Commission.

SEC Shuts Down $600 Million Online Pyramid and Ponzi Scheme.

Scam of The Day

The scam: Consumers are being victimized by con-men who claim that personal bills will be paid by the Federal Government through a new economic development program from President Obama. There is no such program.

Consumers who provide a Social Security Number and credit/debit card information are given fake routing and account numbers to use on a billers website. The biller then attempts to collect payment from a phony account.

In the meantime, the criminals may run up charges on the victim’s credit card or find some other way to wring money from the victim.

Bottom line: The Federal Government does not pay personal bills (at least not yet). Never provide your credit/debit card numbers to anyone UNLESS you initiated the transaction.

About Us

Hometown banking was established in southern Utah with the opening of State Bank of Southern Utah in 1957.

Hometown banking is important because people who live and work in southern Utah make the decisions. Bank employees and officers understand the banking needs of area residents because they are affected by the same economic climate. Find out what hundreds already know - hometown banking is better.

Archives

- June 2015

- May 2015

- January 2015

- December 2014

- October 2014

- September 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- November 2013

- October 2013

- August 2013

- July 2013

- June 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

Tokenization of credit cards is the latest buzz-word in security. One example of Tokenization is in Apple Pay, where your true card number remains hidden during the transaction. Instead, a temporary number issued by your payment network allows your transaction to be processed without revealing your true card number. Even if the one-time number is intercepted, it cannot be used for additional transactions.